In January, more listings came to market, more buyers attempted transactions, and fewer of those attempts made it to closing.

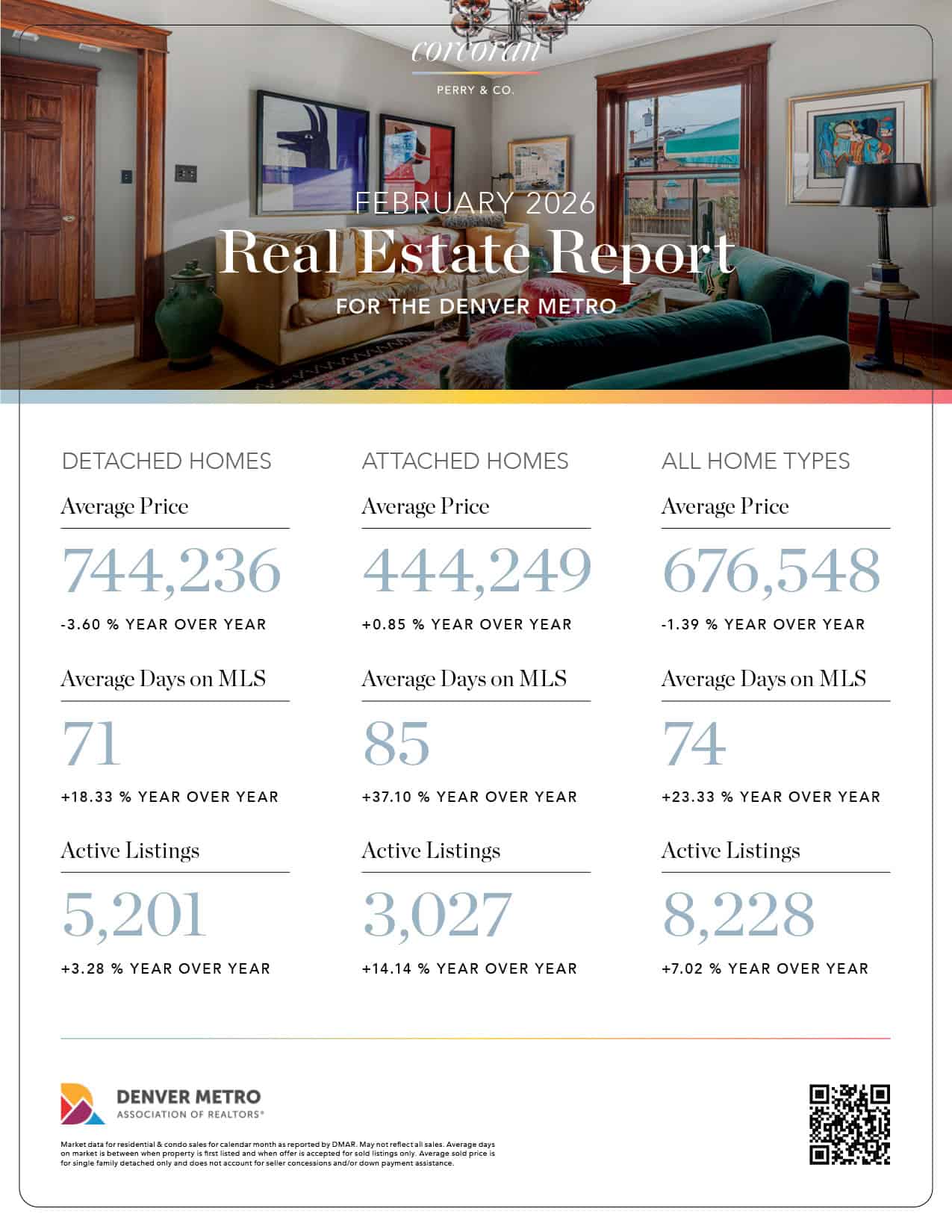

According to the Denver Metro Association of Realtors, active inventory rose to 8,228, up 8.2% month over month and 7.0% year over year… an unusual move for a month that typically contracts. New listings rebounded sharply after year-end withdrawals, pending sales increased seasonally, and yet closed sales fell 40.6% month over month and 19.7% year over year. Average days on market stretched to 74, and median prices declined again, down just under 1% both month over month and year over year.

Contracts opened, stalled, and in many cases dissolved somewhere between inspection and appraisal. Real estate activity exists, but it’s conditional.

Buyers are willing to engage. Sellers are willing to list. What neither side is willing to do anymore is absorb unresolved risk.

Denver Is No Longer One Market

January’s data reinforces a shift that’s been building for several years: Denver no longer behaves like a single housing market.

Detached and attached homes are moving in different directions depending on which metric you’re watching. Attached homes showed softer liquidity: closings fell nearly 40% month over month and more than 30% year over year, while median days on market climbed to 63 days. Yet attached pricing ticked up from December: the median rose to $390,000 (+1.3% MoM) and the average to $444,249 (+3.0% MoM), even as the close-price-to-list-price ratio dipped to 97.6%.

That combination matters. It suggests attached homes aren’t broadly “getting cheaper” so much as clearing at higher price points while lower-confidence inventory lingers or fails to convert. It’s a market that’s selective, not uniformly discounted. It also aligns with what buyers are scrutinizing more closely in attached properties: HOA structure, monthly costs, insurance exposure, and the possibility of future assessments. These factors don’t always show up in the sale price line, but they show up in time on market and conversion.

Detached homes, meanwhile, were weaker on price in January: the median fell to $615,000 (–1.6% MoM) and the average dipped as well, while days on market rose more moderately than in attached segments. Luxury remains selective, often trading on terms that don’t behave like the rest of the MLS. Townhomes tend to fall between these extremes, moving quickly when pricing and HOA terms align, and stalling when they don’t.

At this stage, broad averages conceal more than they reveal. Outcomes depend less on “the market” and more on which segment a property belongs to… and how much friction buyers are being asked to absorb.

Liquidity Is the Constraint

Despite repeated month-over-month price declines, pricing alone is not the limiting factor. Liquidity is.

Listings priced even slightly ahead of buyer tolerance are not politely waiting for spring demand. They are cycling through reductions, re-listings, contract attempts, and terminations. The gap between list-price optimism and clearing prices has widened as buyers grow more comfortable letting misaligned deals fail.

This pattern aligns with statewide data as well. Colorado has now seen several consecutive months of modest price softening paired with suppressed transaction volume. Rather than triggering abrupt repricing, the market is adjusting through incremental erosion and longer timelines.

Pending Sales Rose. Conversion Did Not.

While pending sales rose nearly 47% month over month, that activity did not translate into improved closings. The close-price-to-list-price ratio dipped to 97.9%, reinforcing the widening gap between attempted and completed transactions.

The friction appears mid-transaction: inspections, appraisals, insurance costs, HOA disclosures, and shifting monthly cost assumptions. Buyers are writing offers, but they are increasingly unwilling to renegotiate foundational math.

The market remains effective at generating interest. It is increasingly selective about converting it.

Seller Behavior Is Splitting

Seller behavior has become increasingly polarized.

Motivated sellers (those with clear timelines) are adapting quickly. They are pricing accurately from the start, addressing inspection issues proactively, and resolving uncertainty early.

Discretionary sellers are taking a different approach: pulling listings, waiting for spring, or opting for limited-exposure strategies like private exclusives. While discretion can be appropriate in specific cases, the broader rise of off-market attempts reflects discomfort with open-market price discovery more than strategic advantage.

In a market where liquidity is uneven, limiting exposure rarely changes the outcome. It usually delays it.

Rent Pressure Has Lifted… and Buyer Urgency With It

Rental conditions have shifted materially.

Metro Denver apartment vacancy reached approximately 7.6% by the end of 2025, the highest level in more than a decade, driven by a wave of new multifamily supply. Rent growth has softened, concessions have expanded, and tenant leverage has improved.

That shift removes one of the strongest accelerators of homebuying over the last ten years. First-time buyers are stretching timelines. Renters are renegotiating terms. Fewer purchases are driven by the need to escape rising rents.

Demand hasn’t disappeared. It has slowed and spread out.

Corcoran Perry & Co. Featured Listing: 183 S Kearney Street, Denver CO

Corcoran Perry & Co. Featured Listing: 183 S Kearney Street, Denver CO

What Spring 2026 Is Likely to Test

Spring typically increases participation. It does not automatically increase conversion.

If inventory continues to build faster than closings, incremental price and term adjustments are likely to continue (particularly in attached housing and HOA-heavy segments). If conversion improves through clearer disclosures, better pricing alignment, or shifts in financing conditions, price movement may stabilize.

Several external factors could still alter the trajectory:

- Federal Reserve rate policy and mortgage-rate volatility

- Insurance availability and premium escalation in Colorado

- Labor-market resilience or softening

- Regulatory or lending changes affecting condos and attached housing

Absent a clear catalyst, spring is more likely to clarify market preferences than reverse them.

In the Denver area February housing market, buyers are willing to engage without urgency. Sellers are willing to list without guarantees. What neither side is willing to do is carry unresolved risk through the middle of a transaction. As a result, more deals are being attempted than completed, and outcomes depend increasingly on how quickly assumptions are resolved.

As spring approaches, that condition will matter more than headline volume. Homes that account clearly for price, total cost, and structural risk will convert. Homes that don’t will continue to experience the attention of an attraction, not the commitment of an investment.

Ready to make your next move? Our Denver Real Estate Experts can be your guide.

Gina Cornelison

Socials