At the start of the year, Denver’s housing market signaled cautious participation. The March 2026 Denver housing market report answered back. Pending sales jumped nearly 30% month over month. Closed sales followed. New listings rose both month over month and year over year. Active inventory reached its highest level in some time. And on February 26, the 30-year fixed mortgage rate touched 5.98% (the first time it had closed below 6% since 2022).

According to the Denver Metro Association of Realtors, the March data release moved in the same direction across nearly every metric… a coherence the market hasn’t shown in months. The median close price landed at $580,000, up from January but still 3.3% below last year. Median days in MLS dropped from 53 to 33 in a single month. The close-to-list ratio ticked up to 98.70%.

The question isn’t whether an upswing happened. It did. The question is whether spring can sustain what February started.

The Real Estate Numbers Moved. And the People Will Too.

February’s data was notable less for any single headline than for the direction of the whole. Every major activity metric improved month over month; a rare alignment after an extended stretch of mixed signals.

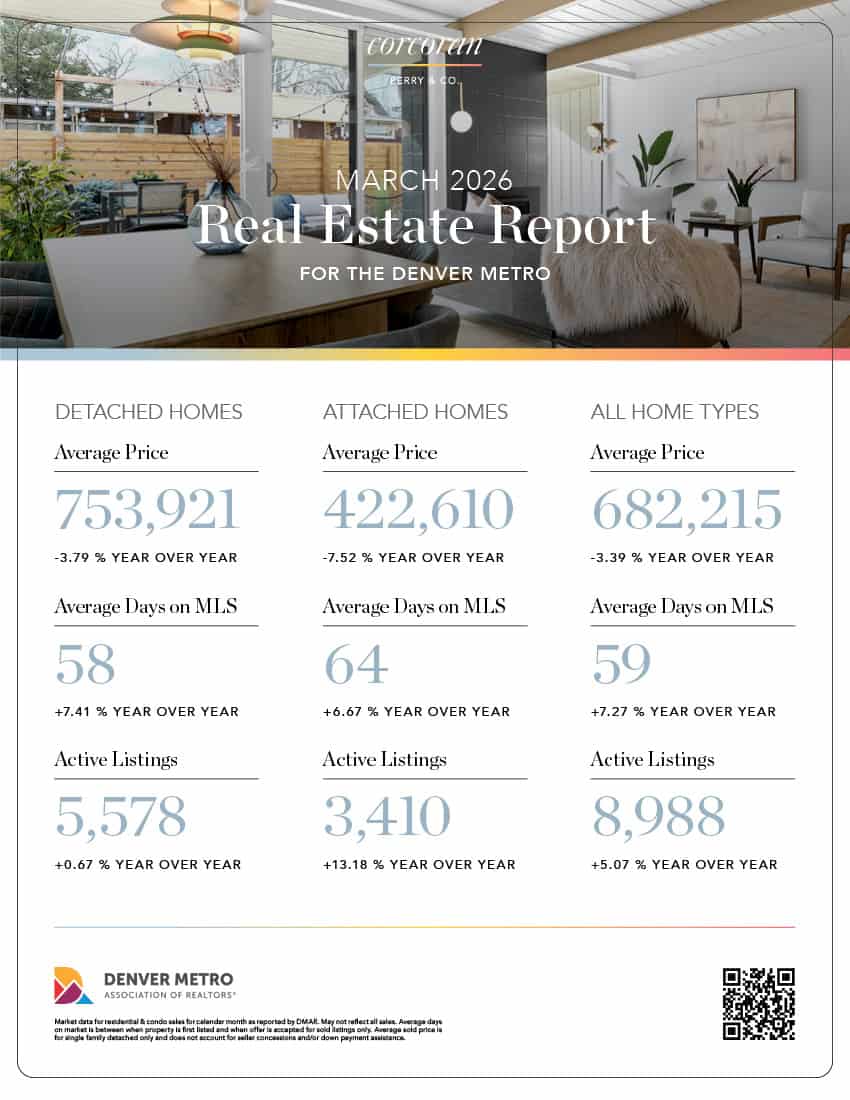

Active listings closed the month at 8,988, up 9.24% from January and 5.07% year over year, which matters because more choice has been one of the things buyers needed to re-engage. New listings came in at 4,995, up 12.15% month over month. Pending sales reached 3,737, a 29.26% month-over-month jump and 15.27% year-over-year gain. Closed sales hit 2,629, up 29.89% from January, with total sales volume reaching $1.79 billion.

Days on market told a similarly pointed story. Average days in MLS fell from 73 to 59, a 19% drop. Median days fell from 53 to 33, a 38% drop. Homes are still sitting longer than they were a year ago, but February compressed timelines in a meaningful way. DMAR Chair, Amanda Snitker, noted that buyers who entered the market early in the year benefited from softer pricing before competition returned, and that competitively priced homes were drawing multiple offers.

Year-over-year comparisons still reflect the overhang from prior years: closed sales are down 6.81% from February of last year, and median price remains 3.33% below year-ago levels. The market is recovering, but it’s recovering from a prolonged correction, not from a brief dip.

Detached and Attached… Still Different Markets

February’s broad improvement did not land evenly. Detached and attached homes continue to behave as separate markets, and the gap between them is wide enough that a single market average obscures more than it explains.

Detached homes closed the month with 2,060 sales and 5,578 active listings, producing a months of inventory (MOI) of 2.71. That’s a seller-leaning number. The highest detached sale of the month was 181 Race St in Denver’s Country Club neighborhood, which sold for $8,595,000 in nine days, cash.

Attached homes tell a different story. With 569 closings and 3,410 active listings, the attached segment sits at 5.99 MOI… just under the 6-month threshold that typically signals a buyer’s market.

The Rate Moment, Years in the Making

On February 26, the 30-year fixed rate touched 5.98%. It was brief (rates have since moved back above 6%), but the moment was not irrelevant. Sub-6% is a psychological threshold for a meaningful share of sidelined buyers, and its appearance likely contributed to the February activity surge.

The forecasting picture for the rest of 2026 points to rates staying in the low-to-mid 6% range. Fannie Mae projects 6.1% for the first quarter; the Mortgage Bankers Association sees low-to-mid 6s through 2026 and into 2027. The practical implication: buyers waiting for a sustained return to the 5s are likely waiting for something that won’t arrive on a predictable schedule.

What the rate environment has shifted, even slightly, is purchasing power. According to NAR analysis, a one-point rate decline opens the market to approximately 5.5 million more qualifying households. That’s not enough to resolve affordability, but it’s enough to move buyers who were close to qualifying across the threshold.

What Price Band You’re In Matters More Than the Market Average

February’s improvement was real, but it wasn’t uniform. Where a property sits in the price distribution still determines more about its outcome than any headline statistic.

In the $500K–$749K range, the spring market is ramping up, though more slowly than in prior years. Buyers in this segment are showing a strong preference for detached homes, in part because HOA cost scrutiny has intensified… not just the monthly fee, but reserve fund health, insurance exposure, and the risk of special assessments. That scrutiny is doing real work at the margin, keeping some attached inventory from converting even when the price looks right.

In the $750K–$999K range, buyers are overwhelmingly choosing single-family homes when they can. The attached product at that range carries nearly 8 months of inventory, and without pricing adjustments, it will continue to sit.

At the top of the market, the dynamics are entirely different. Luxury buyers in Denver are not rate-sensitive in the way mid-market buyers are. Two cash deals above $2.9 million in a single month, both closing in under two weeks, reflect a segment that operates on confidence and availability rather than financing calculus. When the right property is priced correctly, that segment moves.

Corcoran Perry & Co. Featured Listing: 8235 S Jackson Street, Centennial

Corcoran Perry & Co. Featured Listing: 8235 S Jackson Street, Centennial

What the Spring 2026 Denver Housing Market Might Bring

We all thought 2026 was likely to resemble 2025 in its broad shape: healthier inventory levels, steady demand, and continued movement toward balance. That’s a reasonable baseline. But the February numbers introduced a variable that wasn’t in the script (a rate print below 6% and a corresponding surge in activity), and spring will test whether that was a one-month event or the start of a new pattern.

Several variables will shape the answer:

- Whether mortgage rates stabilize below or hold above 6.25% through the spring selling season

- Whether attached inventory finds a pricing floor or continues to accumulate

- Whether labor market conditions in the Denver metro hold firm enough to sustain buyer confidence

- Whether new listing volume continues at the current pace or pulls back as sellers gauge conditions

For March homebuyers, February’s lesson is about timing. The buyers who entered in January and early February captured softer prices before competition returned. As the market accelerates into spring, that window narrows. Homes priced correctly are already drawing multiple offers. And that dynamic is unlikely to reverse before summer.

For spring sellers, February was a reminder that the market is not uniformly forgiving. Detached homes at market-appropriate prices are moving. Attached inventory at the wrong price is not, and more of it is arriving. Precision matters more than optimism right now, and the gap between a well-priced listing and an aspirational one is being measured in months, not days.

The March 2026 Denver Housing Market report answered the early-year hesitation with a genuine movement. Whether that movement compounds or cools is the question spring will answer. In the meantime, the Denver market is selectively competitive, rate-sensitive at the margins, and rewarding preparation over patience.

Ready to make your next move? Our Denver real estate experts can be your guide.

Gina Cornelison

Socials